I remember sitting across the table from a hospital facilities manager three years ago. His backup power system had failed during a summer storm, and he’d spent six hours on emergency protocols while patients were moved to different wings. Now he needed a new Cummins diesel generator—something in the 500kW range—but the quote was sitting at $285,000. He looked at me and said, “I know we need this, but how do we pay for it without wiping out our capital reserves?”

That’s the conversation I’ve had dozens of times in my 12 years working in the power generation industry. A quality commercial generator isn’t a minor purchase. Depending on your power requirements, you’re looking at anywhere from $50,000 for a smaller standby generator to well over $400,000 for industrial-grade units. And that’s before installation, automatic transfer switches, fuel systems, and the inevitable site work.

Here’s what I’ve learned: the upfront cost shouldn’t be your only consideration. The real question is how you structure the purchase to align with your cash flow, maximize tax advantages, and ensure you’re not sacrificing other operational needs. Financing a Cummins generator purchase isn’t just about getting approved—it’s about choosing the right financing structure that works for your business model.

In this article, I’m walking you through everything I wish that facilities manager had known before he started his financing search. We’ll break down equipment financing options, compare leasing against buying, look at what lenders actually care about (hint: it’s not just your credit score), and dig into the tax benefits that can significantly reduce your effective cost. Whether you’re considering Tesla Power, Cummins, Caterpillar, or another brand, the financing principles remain consistent.

Figure 1: Commercial backup power systems represent significant capital investments, typically ranging from $100,000 to $400,000+ for industrial-grade Cummins diesel generators including installation and accessories.

Why Financing Makes Sense for Generator Purchases

Let me be direct: paying cash for a diesel generator rarely makes financial sense, even if you have the money sitting in your business account. I’ve watched too many companies drain their working capital for a generator purchase, only to face a tight situation three months later when they needed funds for inventory, payroll, or an unexpected equipment repair.

The primary argument for generator financing comes down to preserving liquidity. When you tie up $150,000 or $300,000 in a single equipment purchase, that’s money you can’t deploy elsewhere. One manufacturing client I worked with had earmarked $200,000 for a Cummins generator. We structured financing instead, and six months later they used that capital to purchase raw materials when their supplier offered a 15% discount for bulk ordering. The interest they paid on the equipment loan was far outweighed by the savings they captured.

There’s also the tax timing advantage. In 2025, businesses can still leverage Section 179 deductions and bonus depreciation to write off the full cost of qualifying equipment in the year it’s placed into service—even if you’re financing it. You get the immediate tax benefit while spreading the actual cash outlay over 5-7 years. From a pure cash flow perspective, this is one of the most compelling reasons to finance.

Another factor: technology refresh cycles. Backup power systems evolve. Emissions standards change. Control systems improve. If you finance a generator over five years instead of paying cash, you’re better positioned to upgrade when newer, more efficient models come to market. I’ve seen this play out particularly well with data center operators who finance their critical power infrastructure on 3-5 year cycles, ensuring they’re never stuck with obsolete technology.

Finally, financing creates a documented expense stream that makes budgeting predictable. Your CFO knows exactly what the monthly cost is, which makes it easier to forecast, justify to stakeholders, and manage across fiscal years. Compare that to a massive capital expenditure that might blow through your CAPEX budget in a single quarter.

Understanding Equipment Loans and Term Financing

When most people talk about financing a commercial generator, they’re usually referring to an equipment loan or term loan. This is the most straightforward path: a lender gives you the money to purchase the generator, you own it outright from day one, and you repay the loan in fixed monthly installments over a set period—typically anywhere from 24 to 84 months.

What Equipment Financing Actually Covers

One advantage I always point out: equipment financing usually isn’t limited to just the generator itself. You can often bundle the entire project into one loan package. That means the Cummins engine, alternator, sound-attenuated enclosure, automatic transfer switch, fuel tank, installation labor, site preparation, electrical connections, and even your first year of maintenance can all roll into the financed amount. I’ve structured deals where we financed $320,000 for a generator project where the generator itself was $240,000 and the remaining $80,000 covered everything needed to get it operational.

This bundling approach simplifies your life. Instead of coordinating multiple vendors and payment schedules, you’re working with one financing agreement. Your contractor gets paid, your supplier gets paid, and you’re making one monthly payment.

How Equipment Loans Are Structured

Most commercial equipment loans work like this:

- Loan Term: 24-84 months (3-7 years), with 60 months being the most common for generators

- Down Payment: Typically 10-20% of the total equipment cost, though sometimes you can negotiate zero down for strong credit profiles

- Interest Rate: Fixed rates ranging from 6-15% depending on your creditworthiness, time in business, and overall financial health

- Collateral: The generator itself serves as collateral. If you default, the lender has the right to seize the equipment

- Payment Structure: Fixed monthly payments that include principal and interest

Let’s run a real-world example. Say you’re financing $200,000 for a diesel generator set:

Scenario: $200,000 loan at 8% APR over 60 months

- Monthly payment: ~$4,056

- Total interest paid: ~$43,360

- Total cost: $243,360

That $43,360 in interest sounds like a lot until you factor in that you’ve preserved $200,000 in working capital, you can deduct the interest as a business expense, and you’ve potentially written off the entire $200,000 in year one via Section 179.

Term Loans vs. Equipment-Specific Financing

Here’s a distinction that matters: term loans give you a lump sum you can use for various business purposes, while equipment-specific financing is tied directly to the equipment purchase. Equipment financing typically offers better rates because the lender has tangible collateral. If you stop making payments, they repo the generator. With a general term loan, the collateral might be less defined.

For generator purchases, I almost always recommend equipment-specific financing. You’ll get better rates, better terms, and the application process is usually faster because lenders understand the equipment’s resale value and useful life.

The Application Process

Getting approved for an equipment loan isn’t as complex as a commercial real estate mortgage, but you’ll still need to provide:

- Business and personal tax returns (typically 2-3 years)

- Business bank statements (last 3-6 months)

- Financial statements (P&L, balance sheet)

- Equipment quote or invoice showing make, model, price

- Business credit report authorization

- Personal credit check authorization (especially for smaller businesses)

Most lenders move fast once they have everything. I’ve seen approvals in as little as 48 hours for well-documented applications from established businesses. Newer businesses or those with credit challenges might wait 7-14 days.

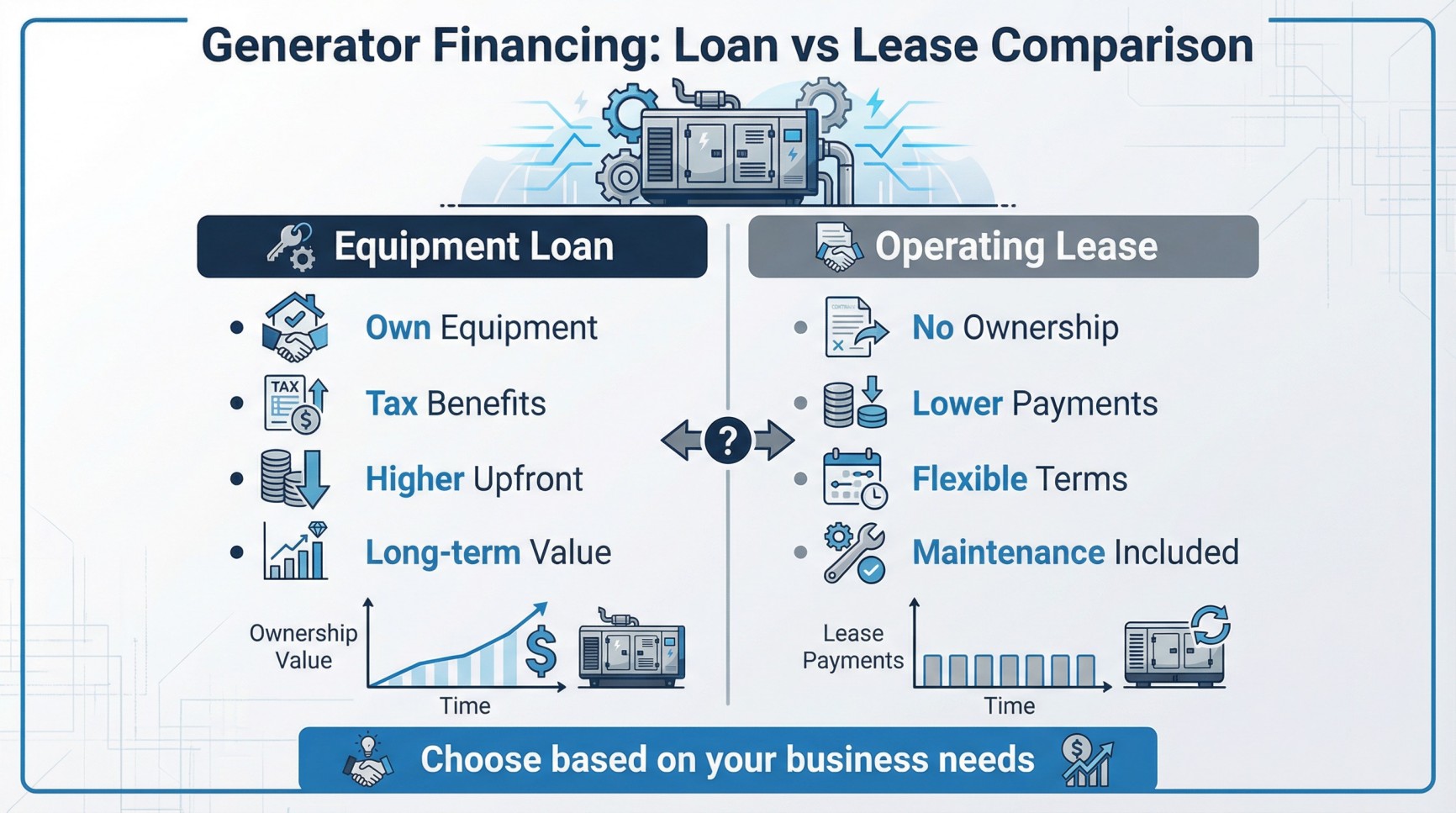

Leasing vs. Buying: What’s Right for Your Business

The lease-versus-buy debate comes up in almost every conversation I have about generator financing. There’s no universal answer, but there are clear scenarios where one makes more sense than the other.

Types of Generator Leases

Operating Lease (True Lease)

In an operating lease, you’re essentially renting the generator for a fixed period—usually 12 to 60 months. You make monthly payments, use the equipment, but never own it. At the end of the lease term, you return the generator, renew the lease, or sometimes purchase it at fair market value.

The advantage: lower monthly payments compared to financing a purchase, and lease payments are typically 100% tax-deductible as an operating expense. The maintenance might be included, which removes your responsibility for service costs.

The disadvantage: you’re paying for equipment you’ll never own. Over time, the total cost exceeds the purchase price. And if your needs are long-term (which they usually are for critical backup power systems), you’re essentially paying rent indefinitely.

Capital Lease (Lease-to-Own)

This is a financing lease structured to transfer ownership at the end. You make payments for 36-72 months, and at the conclusion, you own the generator—either automatically or by paying a small buyout fee (often $1 or 10% of original value).

Functionally, this works almost identically to an equipment loan. Monthly payments are similar, you’re building toward ownership, and the equipment appears on your balance sheet as an asset. The main difference is in how it’s reported for accounting purposes.

When Leasing Makes Sense

I’ve recommended leases in specific situations:

1. Short-Term or Project-Based Needs

If you’re a construction company that needs backup power for a 2-year build, leasing makes sense. You’re not committing to a 10-year ownership of equipment you won’t need when the project wraps.

2. Cash Flow-Sensitive Businesses

If your business is in growth mode and every dollar of capital counts, leasing frees up cash. A hospital expansion project I consulted on used leases for their temporary power during construction, preserving capital for medical equipment that couldn’t be leased.

3. Technology Refresh Strategy

Some businesses—particularly data centers—prefer to lease generators on 3-5 year cycles, upgrading to newer, more efficient models as they become available. You’re always running current technology without the hassle of selling used equipment.

When Buying Makes Sense

Most of my clients buy rather than lease, and here’s why:

1. Long-Term Ownership

A properly maintained Cummins diesel generator can run for 20+ years. If your need for backup power is permanent—manufacturing facilities, hospitals, data centers—ownership is more economical over the equipment’s lifespan.

2. Tax Benefits

Ownership unlocks Section 179 and bonus depreciation benefits that leases don’t offer in the same way. Being able to write off the full purchase price in year one is a huge advantage that you lose with an operating lease.

3. Balance Sheet Asset

Owned equipment is a tangible asset on your balance sheet, which can improve your company’s book value and borrowing capacity for future financing needs.

4. No Restrictions

When you own it, you control it. Lease agreements often have restrictions on modifications, usage hours, and maintenance providers. Own the equipment, and you make the rules.

Comparing Total Cost

Let’s look at a side-by-side comparison for a $200,000 generator purchase:

Financing to Own (60-month term, 8% APR)

- Monthly payment: $4,056

- Total paid: $243,360

- End result: You own a $200,000 asset

Operating Lease (60 months)

- Monthly payment: $3,800 (estimated)

- Total paid: $228,000

- End result: You own nothing

The lease looks cheaper—until you factor in that after 60 months, the financed buyer owns the generator and has zero monthly costs, while the lessee either returns the equipment or continues paying. Over 10 years, buying is almost always more economical for permanent installations.

Key Insight: For critical, long-term power needs, financing to own typically delivers better ROI than leasing. Leases make sense for temporary, project-specific, or short-duration requirements.

Figure 2: Equipment loans and operating leases each offer distinct advantages. Choose based on your long-term power needs, cash flow priorities, and tax planning strategy.

Cummins and Dealer Financing Programs

One financing path that’s often overlooked: going directly through the manufacturer or their authorized dealers. Cummins works with financial partners to offer competitive financing programs, and many Cummins distributors have established relationships with equipment lenders who understand the generator market intimately.

Manufacturer-Backed Financing Advantages

When you finance through a Cummins dealer or their preferred lending partners, you’re working with lenders who specialize in power equipment. They understand the resale value of a Cummins QSX15 or QSK60 engine. They know the typical lifespan, maintenance costs, and depreciation curves. This familiarity often translates to:

- Faster approval times: Because the lender already knows the equipment, they spend less time evaluating whether it’s worth financing

- Better rates: Specialized lenders can offer more competitive terms than general-purpose business lenders

- Flexible structures: Some dealer programs offer deferred payment options, seasonal payment plans for agricultural or seasonal businesses, or step-payment structures that align with your revenue cycles

How Dealer Financing Works

Typically, when you’re working with an authorized Cummins dealer or a brand like Tesla Power, the financing process is embedded into the sale. You discuss your power requirements, they spec out the generator, and when it comes time to talk numbers, they present financing options alongside the cash price.

The dealer doesn’t usually finance the purchase themselves—they partner with banks, credit unions, or specialized equipment finance companies. But because they’ve done hundreds of these deals, the application process is streamlined. I’ve seen dealer-facilitated financing close in as little as 3-5 business days for qualified buyers.

Promotional Financing Offers

Keep an eye out for promotional periods. During slower sales months or at fiscal year-end, manufacturers and dealers sometimes offer special financing incentives:

- 0% financing for 12-24 months: Occasionally you’ll see interest-free financing for shorter terms

- Deferred payments: “90 days same as cash” or “6 months no payments” programs

- Discounted rates: Below-market rates for qualified buyers

I saw a Cummins dealer run a year-end promotion in 2024 offering 5.9% APR for 60 months on generators over $150,000—that was nearly 2 percentage points below market rates at the time. If you’re not in a rush, timing your purchase around these promotions can save significant money.

Comparing Manufacturer Financing to Bank Financing

Should you finance through the dealer or go to your own bank? Here’s how I typically advise clients:

Go with dealer financing if:

- You value convenience and speed

- You’re offered a promotional rate

- You don’t have an established banking relationship for equipment loans

- The dealer’s rate is competitive with what your bank quotes

Go with your own lender if:

- Your bank offers a better rate

- You want to consolidate all business borrowing with one institution

- You’re negotiating a package deal (for example, financing multiple pieces of equipment)

- You have an existing credit line or relationship that gives you leverage

There’s no wrong answer here. I’ve financed generators both ways. The key is to get quotes from multiple sources—the dealer, your bank, and maybe an independent equipment finance company—then compare the total cost over the full term, not just the monthly payment.

SBA Loans and Government-Backed Financing

For small and mid-sized businesses, SBA loans can be a game-changer when financing large equipment purchases like industrial generators. The Small Business Administration doesn’t lend money directly, but they guarantee a portion of loans made by approved lenders, which reduces the bank’s risk and can result in better terms for you.

SBA 7(a) Loans for Generator Purchases

The SBA 7(a) program is the most versatile. You can use these funds for equipment purchases, working capital, or even to refinance existing debt. For a generator purchase, here’s what matters:

- Loan amounts: Up to $5 million

- Terms: Up to 10 years for equipment

- Guarantee: SBA guarantees up to 85% of loans under $150,000 and 75% of loans over $150,000

- Interest rates: Typically more favorable than conventional loans because of the government guarantee

The catch? SBA loans require more paperwork and take longer to close—often 4-8 weeks. But if you qualify and have the time, the rates can be 1-2% below market.

I worked with a medical facility that used an SBA 7(a) loan to finance a $350,000 backup power system. Their interest rate was 7.2% when conventional equipment loans were running 9-10%. Over the 10-year term, they saved nearly $75,000 in interest.

SBA 504 Loans

The SBA 504 program is structured differently. It’s designed for major fixed /assets and involves three parties:

- Conventional lender (bank) provides at least 50% of project cost

- Certified Development Company (CDC) provides up to 40% through an SBA-backed debenture

- Borrower contributes at least 10% down payment

This structure can result in below-market, fixed interest rates for terms of 10, 20, or even 25 years. However, 504 loans are primarily for real estate and long-lived equipment, and they require the purchase to promote business growth or job creation.

For generator purchases, 7(a) loans are more common than 504 loans, but it’s worth asking your lender about both options.

Eligibility Requirements

To qualify for SBA financing, you’ll need to meet these criteria:

- Be a for-profit business operating in the U.S.

- Meet SBA size standards (generally under 500 employees for most industries)

- Demonstrate ability to repay the loan

- Have invested equity in the business

- Exhaust other financing options (SBA loans are intended as a resource of last resort)

That last point is important but often misunderstood. It doesn’t mean you have to be turned down by every bank—it means the SBA loan offers more favorable terms than what’s conventionally available to you.

Should You Pursue SBA Financing?

SBA loans make sense if:

- You’re a small business with limited credit history

- Conventional lenders are quoting high rates or requiring large down payments

- You can wait 6-8 weeks for approval and funding

- You’re financing a large purchase ($200,000+) where a 1-2% rate difference creates meaningful savings

They’re less ideal if you need funding quickly or if you can already access competitive conventional financing.

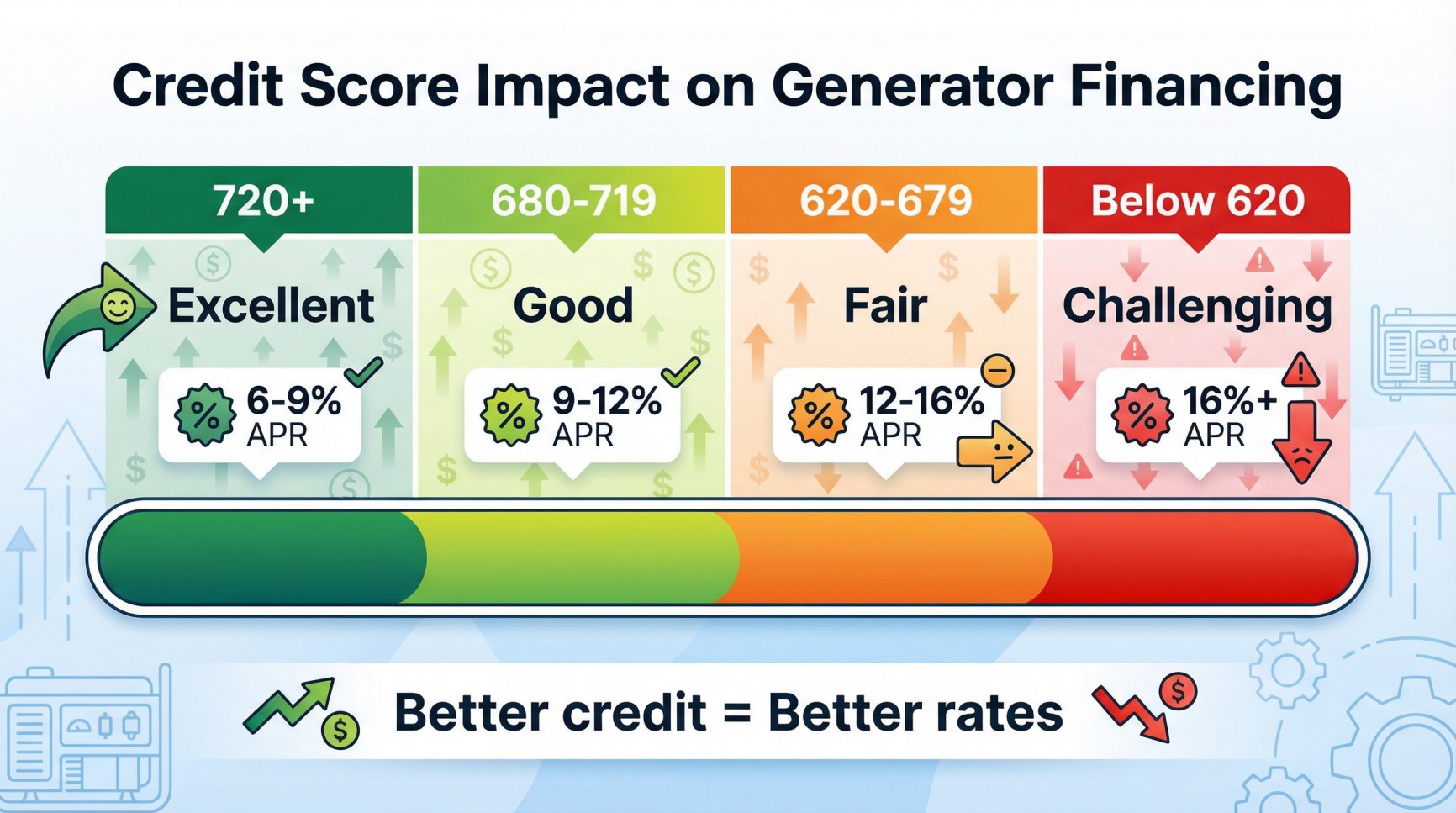

What Lenders Actually Look At (Credit, Revenue, Down Payment)

You might think financing approval is all about your credit score. It’s not. I’ve seen businesses with 780 credit scores get turned down and others with 640 scores get approved. Lenders evaluate a package of factors, and understanding what they weigh helps you present a stronger application.

Credit Score Requirements

Yes, credit scores matter. For commercial equipment financing, here’s the general breakdown:

| Credit Score Range | Approval Likelihood | Typical APR | Down Payment |

| 720+ | Excellent | 6-9% | 0-10% |

| 680-719 | Good | 9-12% | 10-15% |

| 620-679 | Fair | 12-16% | 15-20% |

| 550-619 | Challenging | 16-22% | 20-25% |

| Below 550 | Difficult | 22%+ | 25-30% |

Notice that financing is still possible with scores in the 550-650 range—you’ll just pay higher rates and need a larger down payment. I’ve helped businesses with credit scores in the low 600s secure financing, but it required compensating strengths in other areas.

Figure 3: Your credit score directly influences financing terms. Better credit translates to lower interest rates and reduced down payment requirements for commercial generator purchases.

Time in Business

Most lenders prefer businesses that have been operating for at least two years. Startups or businesses under 24 months face tougher scrutiny. Why? Lenders want to see you’ve survived at least one full business cycle and have established revenue patterns.

That said, newer businesses can still get financing if they have:

- Strong personal credit from the business owner

- Significant down payment (25-30%)

- Contracts or revenue projections showing ability to pay

- Industry experience from the ownership team

Annual Revenue and Cash Flow

Lenders want to know you can afford the monthly payments without straining operations. They’ll look at:

- Annual revenue: Many lenders have minimum thresholds, often around $250,000 for equipment loans over $100,000

- Cash flow: Are you consistently profitable? Do you have positive cash flow after expenses?

- Debt-to-income ratio: Your existing debt obligations compared to your income

- Profitability: Are you cash flow positive? Can you demonstrate consistent profitability?

One metric that comes up frequently: the debt service coverage ratio (DSCR). This measures your ability to pay debt obligations. A DSCR of 1.25 or higher is generally preferred—meaning your cash flow is 125% of your debt payments. If your DSCR is below 1.0, you’re going to face challenges.

Down Payment and Collateral

The size of your down payment directly impacts your approval odds and your interest rate. Here’s why lenders care:

Skin in the game: A 20% down payment means you’re invested. You’re less likely to walk away from the loan.

Loan-to-value ratio: Lenders prefer to lend no more than 80-90% of the equipment’s value. If you default, they want to be able to sell the generator and recover their funds.

Typical down payment expectations:

- Strong credit (720+): 0-10%

- Good credit (680-719): 10-15%

- Fair credit (620-679): 15-20%

- Challenged credit (below 620): 20-30%

The generator itself serves as collateral, but for larger loans, lenders might also place a blanket lien on other business /assets or require personal guarantees from business owners.

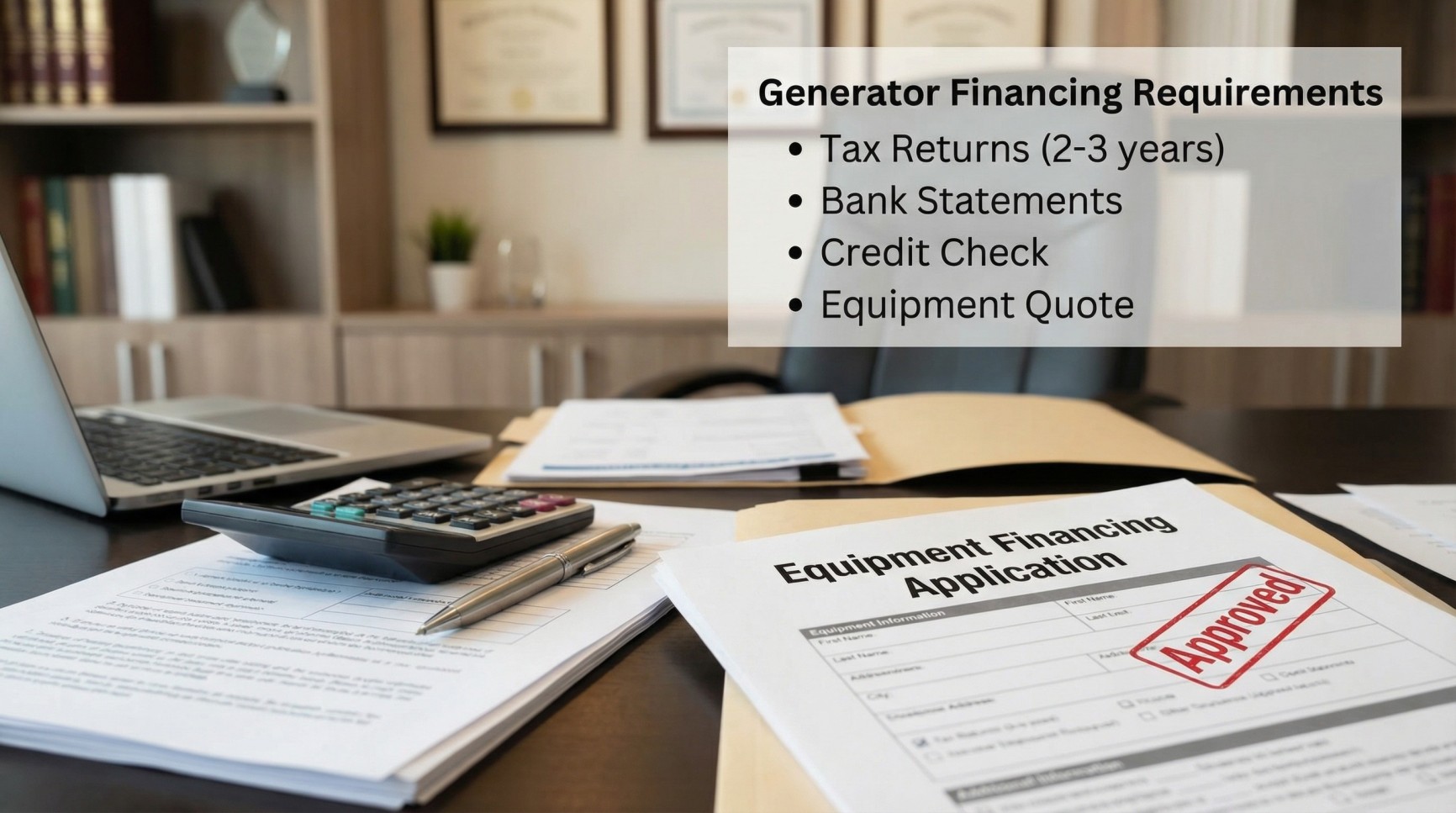

Business Documentation

Be prepared to provide:

- Tax returns: Business and personal, usually 2-3 years

- Bank statements: Last 3-6 months to show cash flow patterns

- Financial statements: Profit & loss statement, balance sheet

- Business plan (for newer businesses): Showing how the generator fits into operations

- Equipment documentation: Spec sheet, quote, or purchase agreement

Pro Tip: Prepare your documentation package before you start shopping for financing. Having everything organized and ready to submit can speed up approval by days or even weeks. Lenders view complete applications as a sign of a well-run business.

Figure 4: Prepare a complete documentation package before applying for generator financing. Having tax returns, bank statements, financial statements, and equipment quotes ready speeds approval significantly.

Current Interest Rates and Typical Loan Terms (2025)

Equipment financing rates have stabilized in 2025 after the volatility of previous years. Here’s where the market stands as of late 2025:

Interest Rate Ranges

For commercial generator financing:

- Excellent credit (720+): 6.5%-9.5%

- Good credit (680-719): 9%-12%

- Fair credit (620-679): 12%-16%

- Below 620: 16%-22%+

These rates assume standard equipment loans with the generator as collateral. SBA loans might offer rates 1-2% lower. Special promotional financing through manufacturers can occasionally dip below 6% for short terms.

Typical Loan Terms

For diesel generators, lenders typically offer:

- Short-term: 24-36 months (higher payments, less interest paid overall)

- Standard term: 48-60 months (most common, balances payment affordability with total cost)

- Long-term: 72-84 months (lower payments, higher total interest cost)

The term you choose should align with your expected equipment lifespan and cash flow needs. A 500kW Cummins QSK19 generator has a useful life of 20+ years, so financing it over 5-7 years makes sense. You’ll own it outright long before it needs replacement.

How Rates Are Determined

Your specific rate depends on several factors:

- Creditworthiness: Your business and personal credit scores

- Time in business: Established businesses get better rates than startups

- Down payment: Larger down payments reduce lender risk, lowering your rate

- Loan term: Shorter terms often have slightly lower rates

- Equipment type: Generators from reputable brands like Cummins, Tesla Power, Caterpillar, or Kohler command better financing terms than unknown brands

- Lender type: Banks, credit unions, and specialized equipment lenders all price differently

Fixed vs. Variable Rates

Most equipment financing uses fixed interest rates, which means your rate stays constant throughout the loan term. This is ideal for budgeting—you know exactly what you’ll pay every month.

Variable rate options exist but are less common for equipment loans. Unless you’re extremely confident rates will drop significantly, fixed rates provide better predictability for business planning.

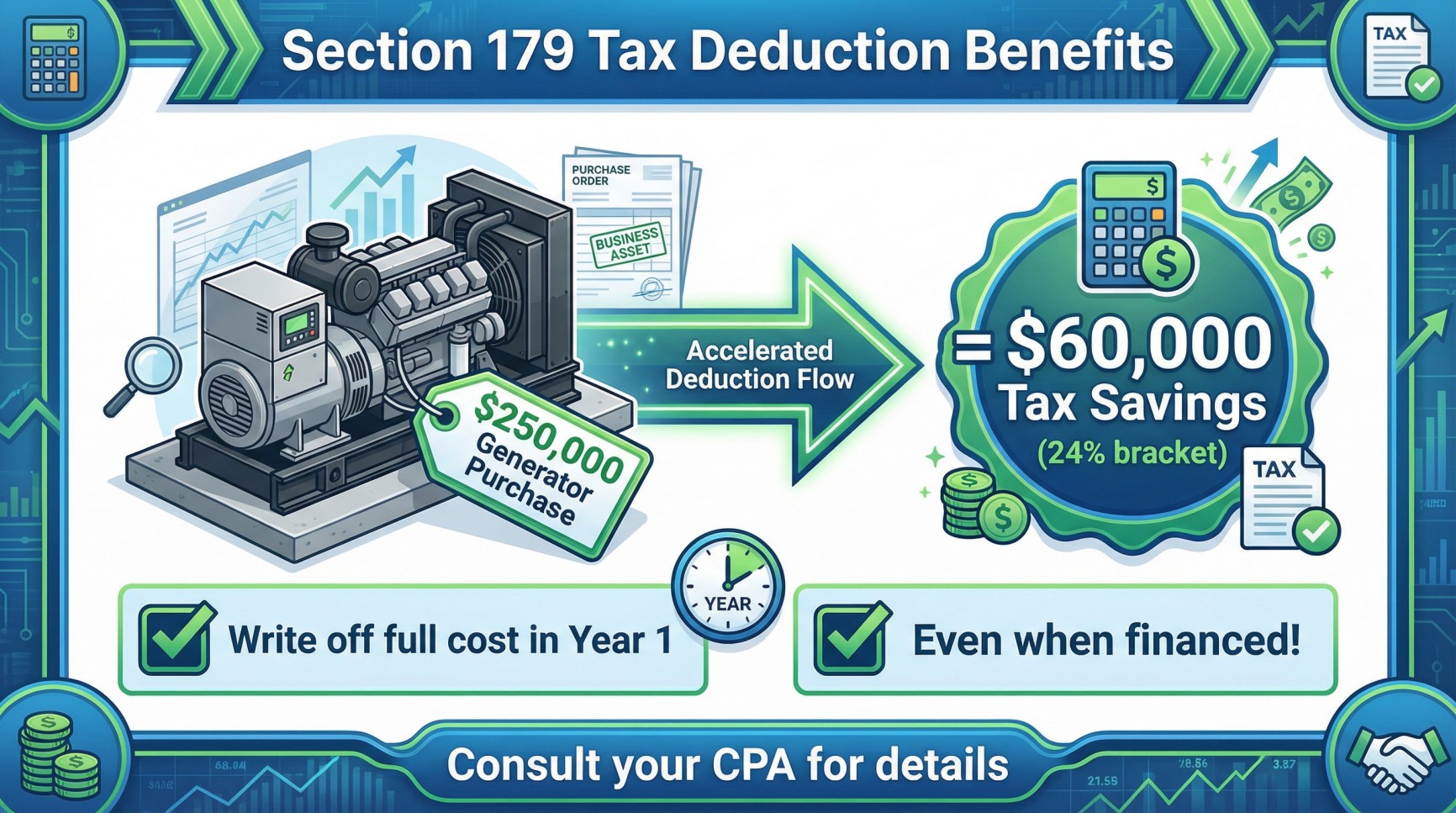

Tax Advantages: Section 179 and Bonus Depreciation

This is where financing a generator gets really interesting from a financial standpoint. The tax benefits available in 2025 can dramatically reduce the effective cost of your purchase, even when you’re financing rather than paying cash.

Section 179 Deduction Explained

Section 179 of the IRS tax code allows businesses to deduct the full purchase price of qualifying equipment in the year it’s placed into service, rather than depreciating it over several years. For 2025, this is particularly advantageous.

Here’s what you need to know:

- Maximum deduction: Section 179 limits have been updated for 2025 (consult your tax advisor for current limits)

- Equipment must be used more than 50% for business purposes

- The generator must be purchased and operational by December 31, 2025 to qualify for the 2025 tax year

- You can claim this deduction even if you financed the purchase

That last point is crucial. You don’t need to pay cash to take the full deduction. If you finance $300,000 for a backup generator system, you can potentially write off the full $300,000 on your 2025 taxes—even though you’re making monthly payments.

Real-World Tax Benefit Example

Let’s say you’re in the 24% corporate tax bracket and you purchase a $250,000 Cummins diesel generator:

Without Section 179:

- You’d depreciate the equipment over 7-15 years

- Year 1 tax benefit: ~$17,857 (using MACRS depreciation)

- Tax savings: ~$4,286

With Section 179:

- You deduct the full $250,000 in year 1

- Tax savings: ~$60,000

That’s a $60,000 reduction in your tax bill in the first year. If you financed the generator at 8% for 60 months, your monthly payment is ~$5,070. That $60,000 tax savings covers almost your first 12 months of payments.

Bonus Depreciation in 2025

In addition to Section 179, bonus depreciation has been reinstated at 100% for qualifying property in 2025. This allows businesses to deduct the full cost of equipment in the first year.

How this works with Section 179: typically, you’d apply Section 179 first to get the most favorable treatment. If your equipment cost exceeds Section 179 caps, you can then apply bonus depreciation to the remaining amount. This combination can allow for a near-total write-off of even very large generator purchases.

Who Benefits Most?

Businesses that benefit most from these tax incentives:

- Profitable companies with significant tax liability: If you’re paying substantial taxes, accelerated depreciation reduces that burden immediately

- Businesses making large equipment purchases: The bigger the purchase, the bigger the tax savings

- Companies with strong year-end cash flow: You capture the tax benefit in year 1 while spreading payments over 3-7 years

Important Considerations

A few things to remember:

Timing matters: The equipment must be purchased AND placed in service by December 31 to qualify for that tax year. Given generator lead times (which can be 8-16 weeks for large units), plan ahead.

Consult your tax advisor: Tax law is complex and your specific situation matters. A CPA can help you structure the purchase to maximize benefits.

Recapture rules: If you sell or dispose of the equipment within a certain timeframe, you may need to recapture some of the depreciation benefits. This rarely applies to generators, which are typically long-term /assets.

Business use requirement: The generator must be used primarily for business purposes. If it’s providing backup power to a mixed-use facility, document the business percentage carefully.

Tax Savings Summary: When you combine Section 179 and bonus depreciation with financed payments, you get the best of both worlds—immediate tax benefits while preserving working capital. For many businesses, the tax savings in year 1 effectively offset 20-40% of the equipment’s cost.

Figure 5: Section 179 tax deductions can dramatically reduce the effective cost of your generator purchase. Write off the full equipment cost in year one, even when financing, creating immediate tax savings that can offset 20-40% of the investment.

Calculating ROI and Justifying the Investment

When you’re financing a $200,000-$400,000 diesel generator, someone’s going to ask: “What’s the return on investment?” Whether it’s your CFO, your board, or your business partner, you need to articulate why this makes financial sense.

The Cost of Downtime

The most compelling ROI argument for backup power is downtime avoidance. What does a power outage cost your operation?

For a manufacturing plant running three shifts, even four hours of downtime might mean:

- Lost production: $50,000-$150,000

- Spoiled materials or work-in-progress: $20,000-$75,000

- Labor costs (workers standing idle but still paid): $10,000-$30,000

- Customer penalties for missed deliveries: Variable

- Equipment damage from improper shutdown: $25,000+

One outage could cost more than the generator itself. If you experience just one significant outage every 3-5 years, a backup generator pays for itself.

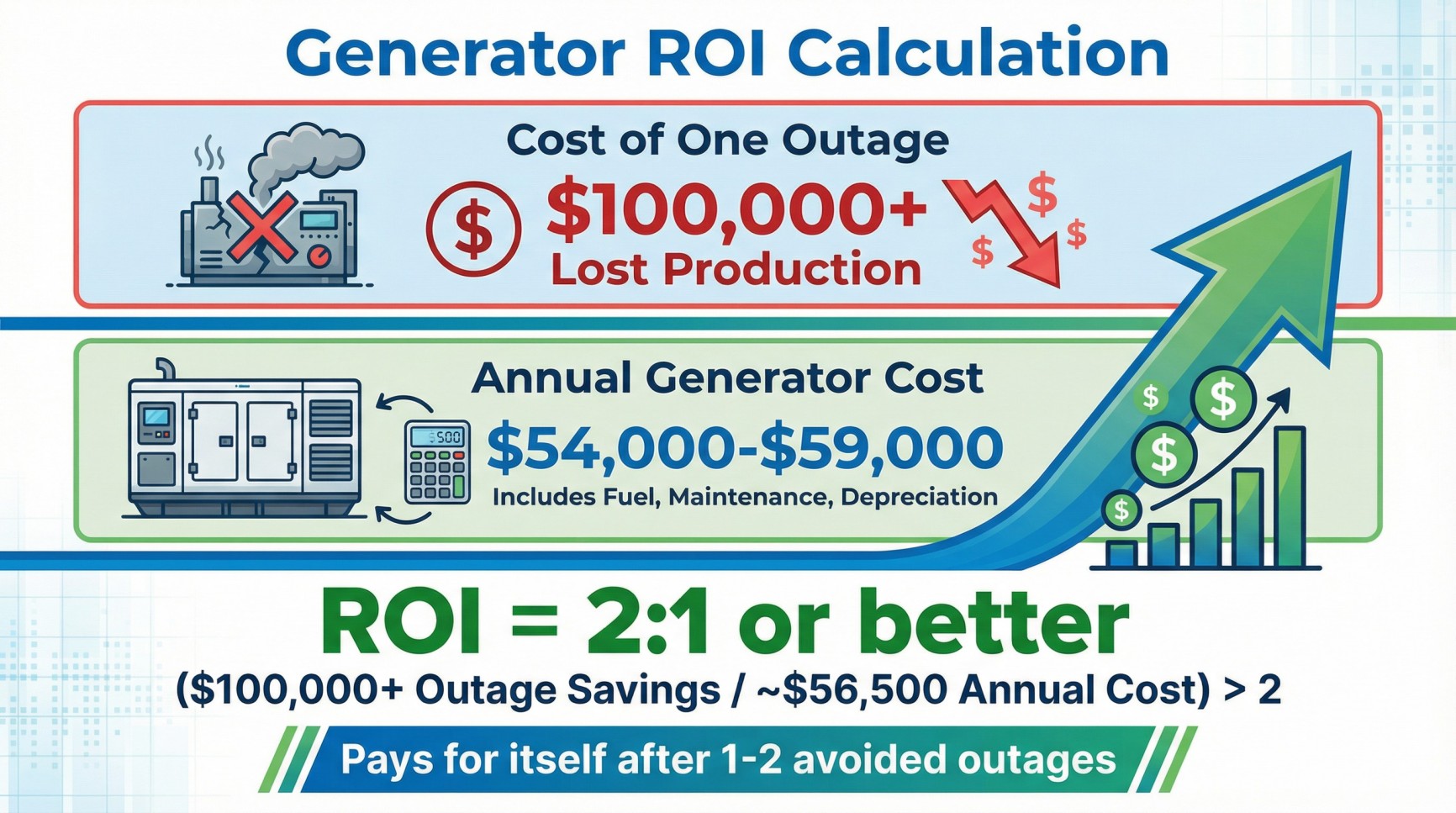

Figure 6: Return on investment for backup generators is compelling when you factor in downtime avoidance. One prevented outage often pays for a year or more of financing costs.

ROI Calculation Framework

Here’s how I help clients calculate generator ROI:

Annual Cost of Ownership:

- Financing payment: $4,056/month × 12 = $48,672/year

- Maintenance and service: $3,000-$6,000/year

- Fuel for testing (monthly run cycles): $1,200-$2,400/year

- Insurance: $800-$1,500/year

Total annual cost: ~$54,000-$59,000 for a $200,000 financed generator

Annual Benefit:

- Downtime avoided: Depends on your outage frequency and cost per hour

- Insurance premium reductions: Some insurers offer discounts for backup power

- Business continuity value: Maintaining customer relationships, avoiding penalties

- Competitive advantage: Ability to guarantee uptime to customers

If one avoided outage per year saves you $100,000, your ROI is nearly 2:1 annually.

Soft Benefits

Don’t overlook intangible benefits:

- Customer confidence: Being able to promise uninterrupted service

- Employee morale: Not sending workers home during outages

- Regulatory compliance: Some industries require backup power

- Business resilience: Weather events, grid instability, planned utility work

Justifying the Investment to Stakeholders

When presenting to decision-makers:

- Lead with risk: “We experienced X hours of downtime last year costing $Y. One major outage cost us $Z.”

- Show the math: Present total cost of ownership against downtime costs

- Highlight tax benefits: “The Section 179 deduction reduces our net cash outlay to $X in year 1”

- Compare to alternatives: Temporary rental generators cost $5,000-$15,000 per month and aren’t always available during widespread outages

- Frame as insurance: “We pay $X,000 annually for property insurance. This is operational insurance that also provides ROI.”

How to Get Better Rates and Terms

You don’t have to accept the first financing offer you receive. Here’s how to negotiate better terms:

Get Multiple Quotes

Always obtain at least three quotes:

- Dealer/manufacturer financing

- Your primary business bank

- An independent equipment finance company

More competition means better leverage. When lenders know you’re shopping around, they sharpen their pencils.

Improve Your Leverage

Larger down payment: If you can afford 20-25% down instead of 10-15%, use that to negotiate a lower rate. A $40,000 down payment on a $200,000 generator might reduce your rate by 0.5-1.0%, saving thousands over the loan term.

Shorter term: Willing to do 48 months instead of 60? That reduced risk often translates to a lower rate.

Strong financial documentation: Present a complete, organized application package. Lenders reward well-prepared borrowers with better terms.

Timing Your Purchase

End of quarter or end of year can work in your favor. Dealers and lenders have sales targets, and they’re more motivated to close deals in the final weeks of their fiscal periods. I’ve seen clients negotiate an extra 0.5% off by timing their purchase for late December.

Negotiation Points Beyond Interest Rate

Don’t fixate solely on the rate. Other negotiable terms:

- Prepayment penalties: Ensure there’s no penalty if you want to pay off the loan early

- Payment schedule: Some lenders offer quarterly or seasonal payment structures

- Grace periods: Negotiate 30-60 days before first payment (allows time for installation and commissioning)

- Bundled services: Can maintenance contracts be rolled into financing?

Comparing Financing Across Brands (Cummins, CAT, Generac, Kohler)

Financing availability and terms can vary by manufacturer. Here’s what I’ve observed across major brands:

Cummins

Cummins has robust dealer networks with strong financing relationships. Their widespread market presence means lenders are comfortable with Cummins equipment values. Expect competitive rates and straightforward approval for standard commercial applications. Cummins units from 20kW to 3,000kW all finance similarly based on your creditworthiness rather than equipment type.

Caterpillar (CAT)

Caterpillar generators command excellent financing terms, particularly for large industrial installations (500kW+). Cat Financial, their lending arm, offers competitive programs. The brand’s reputation for durability means strong resale values, which translates to better loan-to-value ratios and potentially lower down payments.

Generac

Generac dominates the residential and light commercial market but also produces larger commercial units. Financing for smaller Generac units (under 150kW) is readily available through dealer networks and general equipment lenders. For larger industrial Generac units, you’ll find similar terms to Cummins and Cat.

Kohler

Kohler generators finance well across their range. The brand’s long history and solid reputation mean lenders view them as reliable collateral. Kohler dealer financing programs are competitive, though not always as aggressive as Cat Financial.

Tesla Power

Manufacturers like Tesla Power offer Cummins-powered generators and often work with equipment finance partners who understand their product quality. Because many use recognized engine platforms (Cummins, Perkins, etc.), lenders evaluate them based on the engine brand reputation plus the overall build quality and warranty support.

The Bottom Line on Brand Financing

Honestly? For established brands, financing terms are more dependent on your financial profile than the generator brand. A buyer with 750 credit and strong cash flow will get excellent rates on any reputable brand. The brand primarily affects:

- Lender familiarity: More recognized brands mean faster approvals

- Resale value assumptions: Affects loan-to-value ratios

- Manufacturer financing programs: Some brands offer promotional rates

Focus less on “which brand finances best” and more on “which generator meets my technical requirements at a price point I can afford.”

Making Your Financing Decision

You’ve now seen the full landscape: equipment loans, leasing options, SBA programs, dealer financing, approval factors, current rates, tax benefits, and brand comparisons. So how do you actually make the decision?

Start with your technical requirements. What power capacity do you need? What’s your runtime requirement? Are there fuel preferences, emissions standards, or space constraints? The generator needs to solve your power problem first—financing is secondary.

Once you’ve spec’d the right generator (or narrowed it to 2-3 options), get quotes for both equipment and financing. Most dealers will provide turnkey quotes including installation, transfer switches, and financing options.

Then run the numbers:

- Total cost over the loan term: Don’t just compare monthly payments

- Tax benefits: Factor in Section 179 and depreciation

- Cash flow impact: Can you afford the payments without straining operations?

- Opportunity cost: What else could you do with the capital if you finance instead of paying cash?

For most businesses with solid fundamentals, financing makes more sense than cash purchase. The combination of preserved liquidity, tax benefits, and predictable payment structures outweighs the interest cost.

If you’re still uncertain, consult with both your CPA (for tax implications) and your banker or financial advisor (for cash flow analysis). A $200,000-$400,000 decision deserves professional input.

The generator investment itself is smart—it’s insurance against downtime, protection for your operations, and often a requirement for business continuity. Financing it properly ensures you get that protection without compromising your financial flexibility.

Frequently Asked Questions

1. Can I finance a generator with bad credit?

Yes, but it’s more challenging and expensive. With credit scores below 620, you’ll face higher interest rates (16-22%+) and larger down payment requirements (20-30%). Some specialized lenders work specifically with challenged credit situations. Your best approach: improve your application with a larger down payment, strong business financials, and documented cash flow. Consider SBA 7(a) loans, which are more forgiving of credit issues if you can demonstrate business viability. Alternative lenders and equipment finance companies may approve deals that traditional banks won’t, though at premium rates. If possible, work on improving your credit score for 6-12 months before applying—even a 40-50 point increase can significantly impact your terms.

2. How long does generator financing approval take?

Timeline varies by lender and loan type:

- Dealer financing: 2-5 business days for straightforward applications

- Bank equipment loans: 5-10 business days

- SBA loans: 4-8 weeks due to additional paperwork and government guarantee process

- Specialized equipment lenders: 3-7 business days

The key variable is documentation completeness. Applications with all required documents (tax returns, financials, equipment specs) process much faster than incomplete submissions. Expect the entire process from application to funding to take 2-4 weeks on average. If you need power quickly, communicate your timeline upfront—some lenders offer expedited processing.

3. What down payment do I need for a Cummins generator?

Typical down payments range from 0-30% depending on your credit profile:

- Excellent credit (720+): 0-10% down, sometimes zero with strong financials

- Good credit (680-719): 10-15% down

- Fair credit (620-679): 15-20% down

- Challenged credit (below 620): 20-30% down

For a $200,000 generator, you might need $0-$60,000 down depending on your situation. The down payment reduces the lender’s risk and typically results in better interest rates. Even if you qualify for zero down, consider putting 10-15% down to reduce your monthly payments and total interest cost. Some buyers use the tax savings from Section 179 to effectively cover their down payment in the first year.

4. Is it better to lease or buy a commercial generator?

For most permanent installations, buying is better from a long-term financial perspective. Here’s why:

Buy if:

- You need backup power for 10+ years (most common scenario)

- You want to capture Section 179 and depreciation tax benefits

- You want the generator as a balance sheet asset

- You prefer lower total lifetime cost

Lease if:

- You have short-term or project-specific needs (2-3 years)

- You want to refresh technology every 3-5 years

- You prefer lower monthly payments and off-balance-sheet financing

- Maintenance is included in the lease (reduces your operational burden)

For critical backup power at hospitals, manufacturing facilities, data centers, or any business with permanent power needs, financing to own delivers better ROI over the equipment’s 15-25 year lifespan.

5. Can I include installation costs in generator financing?

Yes, absolutely. Most equipment financing packages allow you to bundle the complete project:

- Generator equipment purchase

- Automatic transfer switch (ATS)

- Fuel tank and fuel system

- Installation labor and site work

- Electrical connections and switchgear

- Permits and inspections

- Initial maintenance contracts

Bundling everything into one loan simplifies your payment structure and ensures you have complete funding for a turnkey installation. I typically recommend financing 100% of the project cost rather than trying to separate equipment purchase from installation. Lenders understand that installation is necessary for the equipment to function, so they’re usually comfortable including it. Just make sure your equipment quote clearly itemizes all components so the lender can see exactly what they’re financing.